A leading reinsurance hub in Europe

Luxembourg is the largest captive reinsurance market in the EU. International companies from all over the world have established around 200 reinsurance undertakings in the Grand Duchy.

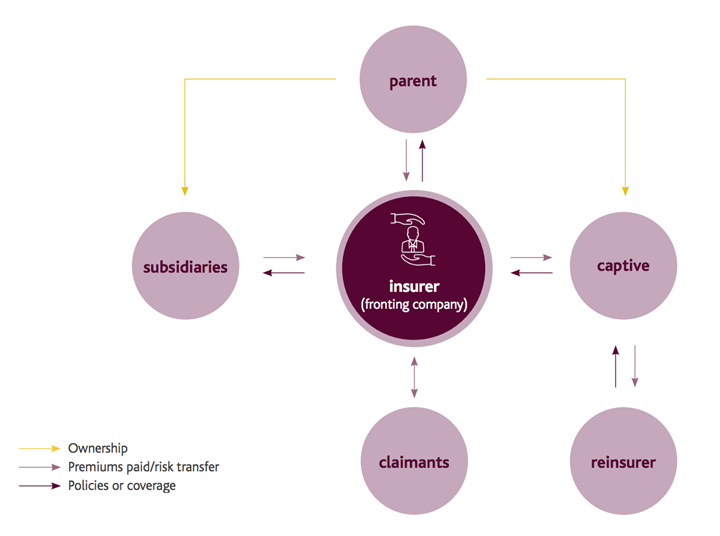

There are several benefits of captive reinsurance. The premiums paid to the captive by the parent and affiliates of the group and the attached captive’s underwriting profits can be retained within the international group and used to finance the business activities of the other subsidiaries of the group.

The captive reinsurance, being an “in-house” reinsurance solution, allows its owner to tailor the insurance to suit the group’s specific requirements. In particular, international groups with different types of risks in different geographic locations may often have to purchase insurance policies from local providers. A captive can create a “one-stop shop” within the group, enabling the owner of the captive to allocate deductibles for each risk or territory.

The captive also centralises the risk management strategy of the international group, allowing for a better overall assessment of the group’s risk exposure and losses.

The role of reinsurance in the transfer of insurance risk

For several decades, Luxembourg has stood out as a financial centre specialised in fund management. However, it is also a well-established big captive reinsurance hub and many of these captive reinsurance companies are also clients of major insurers.

The vast majority of reinsurance companies in Luxembourg are of the “captive” type which means they are subsidiaries of international groups and their principal objective is that of reinsuring the risks of the other companies in the group. Captive reinsurance is essentially an “in-house” insurance entity created to insure the parent company and its affiliated companies.

There is no difference in the European and Luxembourg domestic legislation between standard reinsurance companies and captives, both in terms of activities and taxation, but a captive largely restricts its activities to reinsuring other members of its group. Both captives and non-captives operate in a regulatory framework defined at the EU level by the Reinsurance Directive, transposed into Luxembourg legislation in December 2007, and by the Solvency II Directive, transposed in December 2015.

INSURANCE:

A LEADING FINANCIAL CENTRE IN EUROPE

-

A LEADING FINANCIAL CENTRE IN EUROPE Weiter lesen

-

INSURANCE IN LUXEMBOURG Weiter lesen

-

LUXEMBOURG LIFE INSURANCE Weiter lesen

-

LUXEMBOURG LIFE INSURANCE Weiter lesen

-

LUXEMBOURG NON-LIFE INSURANCE Weiter lesen

-

LUXEMBOURG REINSURANCE Weiter lesen

-

FUTURE CHALLENGES FOR THE INSURANCE INDUSTRY Weiter lesen