A perhaps less well-known effect of the 2008 global financial crisis was the large contribution it played in the manner in which high net worth individuals (HNWI) invest. Since the 2008 crisis, the wealth held by these individuals has more than doubled, as has their share of global wealth. In fact, HNWI wealth grew at impressive 7.7% compound annual growth rate between 2008 and 2020, far above the 4.27% seen in the decade prior to the 2008 crisis. A large reason for this growth is the shift in the way that HNWI are putting their money to work.

Policies initiated post the financial crisis created an era of low-yielding debt.

Bonds and equities remain the core assets of any portfolio, however according to Maria Nemekh, CFA, Investment Advisor at Banque de Luxembourg, from 2010 onwards a new era of investing emerged. “It’s defined by a booming US economy, a bull run in the stock market, and a decline on fixed income yields. Why did this happen?

The vast measures implemented due to the Covid crisis further aggravated this phenomenon.

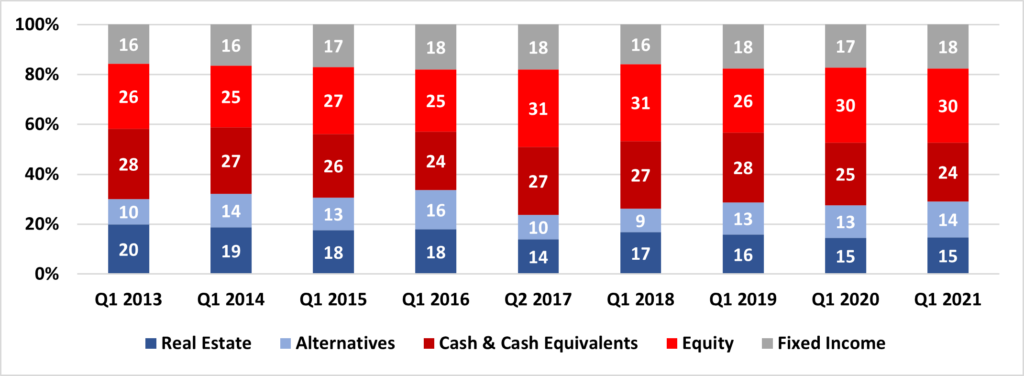

As investors sought to avoid capital erosion, allocations to real assets, in this case equities, rose significantly (cf. Figure 1). Clients have also had so diversify geographically, especially given as European equities by-and-large underperformed in contrast to the overall market. Given this there is less of a home bias when investors look to put their money to work.

HNWI Asset Allocation (%)

Emilie Serrurier-Hoël, Head of Wealth Management at Banque Internationale à Luxembourg, notes however that while geographic diversification is important, clients still demand stability. “Clients have looked at emerging markets for many years, thinking that this might be the year, however long-term it never panned out and in the end investors continue to search for stability in US and European equities.”

Clients have looked at emerging markets for many years, thinking that this might be the year, however long-term it never panned out and in the end investors continue to search for stability in US and European equities.

What in real estate might be “location, location, location” in asset allocation has become “quality, quality, quality”. While wealth managers advocate for a number of factors, including sectoral diversification, market cap diversification, and geographic diversification, the number one factor remains high quality companies. For Nemekh this means “companies with a transparent and clear business model, solid balance sheet, high margins and return on capital, the capacity to generate consistent cash flow, and which are price makers.”

Alongside the shift to equities, exposure to fixed income has decreased significantly among portfolios in recent years. Compared to the figures in the table above, in 1998 fixed income accounted for 36% of HNWI’s total portfolio, in 2002 at 30%, and in 2006 at 21%. Clear then there is a need to find a “replacement” for the asset class. Two key factors are important when doing so, namely a lower volatility to equity and the ability to provide alpha during times of crisis. This has seen gold and other metals take a more prominent place, as well as liquid alternative strategies, such as hedge funds.

The demand is clear and many of our clients are tempted, however it is our role to educate our clients on the risks, from the lock-up period, possible liquidity issues, and the increased risk relating to these products.

Alternatives however often represent a significantly more complex and risky investment environment. Serrurier-Hoël, for example, notes however that when turning to alternatives, it is important to find a balance. While many UHNWI clients have strong networks and the ability to “go-it-alone”, accessing the asset class via direct investments, it’s important that the bank acts as an advisor ensuring that the client is not taking significant risk. “The demand is clear and many of our clients are tempted, however it is our role to educate our clients on the risks, from the lock-up period, possible liquidity issues, and the increased risk relating to these products.”

Here alternative funds can offer a solution or a sort of middle ground. “By offering a lower minimum investment amount, better connections with GPs, knowledge and experience, funds provide investors with a larger selection of deals and increased transparency due to various frameworks,” explains Nemekh.

Alongside the rush into equities there is clear demand for private assets. However, a notable risk emerges due to the crowding effect. Many portfolios now consist of the exact same assets, both listed and unlisted. This can be further exacerbated by the increasing use of leverage. Looking at listed assets, Microsoft, Meta, Apple, Amazon and Alphabet represent approximately 38% of the NASDAQ and 24% of the S&P500. “Active management plays an important diversifying aspect in this case,” highlights Nemekh.

An additional layer that adds complexity to the role of wealth managers comes in the for of ESG. There is no doubt that sustainability has become embedded within HNWIs portfolios. While investor demand initially drove the sustainability demand, the shift in Europe has now been formalised with the various regulatory packages relating to this deal. These have in turn ensured that companies within the real economy improve their ESG profiles or they could find themselves with decreased market-based financing.

“Our role as investment professionals is not only to invest in companies with the best ESG credentials, but also to push the laggards and encourage them to improve those metrics,” says Nemekh. The challenge comes in manufacturing appropriate products however, as Serrurier-Hoël highlights, with sustainability data and meeting clients demand for maximising impact becoming increasingly challenging.

Despite this, the challenges, high net worth clients are increasingly calling for sustainable investments. Both Nemekh and Serrurier-Hoël noted that clients want to ensure they are position their money in the right place. The long-term perspective allows them to maximise the impact of their investments.

Another area in which one might expect growing interest from younger clients is digital assets, however as Serrurier-Hoël puts it: “It’s not only the younger generation. Requests come from all client groups, especially relating to the more well-known coins such as Bitcoin.” However, Serrurier-Hoël and Nemekh both highlight that these assets do not align with their banks’ investment thesis.

“Our role is, as an advisor, to accompany our clients in terms of understanding and of course we monitor the trends, but given the volatility of the asset class, it doesn’t correspond to our philosophy,” Serrurier-Hoël explains.

The more interesting aspect rather stems from the innovations underlying decentralised finance, such as blockchain, tokenisation, and others. “Looking forward ten to twenty years, these will change the landscape of the global financial industry,” Serrurier-Hoël states. At the same time, macroeconomic shifts are likely to change the way that HNWI have put their money to work in recent years.

Our role as investment professionals is not only to invest in companies with the best ESG credentials, but also to push the laggards and encourage them to improve those metrics.

Inflation, at a level not seen in previously in the Eurozone, is worrisome for HNWIs and is shifting mindsets and asset allocation. Hedging inflation risk is also not something that has been a large part of portfolios in recent years and is likely to increasingly become key. In this environment, it’s likely to see further shifts out of cash and into different asset classes, such as real estate.